Chapters:

- Introduction

- Price System and Voluntary Exchange

- Property Rights, the Rule of Law, and Contracts

- Helping Others and the Profit Motive

- Conclusion

- Glossary

Price System and Voluntary Exchange

Perhaps you've heard the phrase Invisible Hand, but weren't sure what it meant. A Scottish philosopher named Adam Smith coined the phrase in the 18th century. He used it to describe the lack of formal coordination between buyers and sellers in a free market.

No one tells the supermarket owner what to carry, no one tells the farmer what to grow or how to grow it, no government overseer tells the truck driver what loads he should haul. Yet all those people somehow work together in harmony to provide us with a steak dinner. That's the Invisible Hand at work.

Click on this video for a brief overview of signaling in the marketplace:

Part of what makes up the voluntary exchange of goods and services for money is the idea of marginal decision-making. Marginal decision-making in economics refers to the idea that people will make decisions about what to buy or sell. They do this based on the benefit(s) received and cost(s) incurred of buying or selling just one more given product or service. Buyers rely on marginal utility, the value of satisfying a need by buying just one more product or service. Sellers rely on marginal cost, the cost of making one more product or service. Both buyers and sellers rely on these to help them decide what and how much to buy or sell.

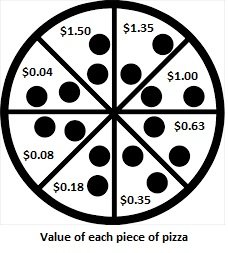

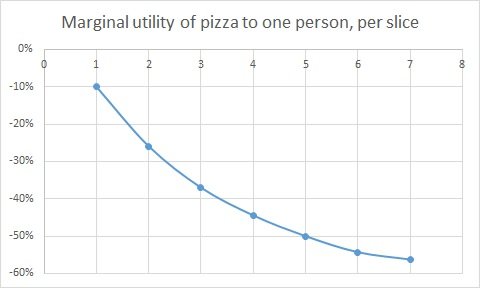

Let's expand on marginal utility. This concept is important to buyers because we are limited in how many goods and services we can buy to satisfy our needs. Since we also have limited means - such as money earned from working and saving - we have to make choices about how we will meet as many needs as we can. Take a pizza, for example. Suppose you are hungry and you see a place offering 8 slices of pizza for $5.12. How valuable is that pizza to you? Well, it satisfies one of the basic needs: hunger. The first piece of pizza really satisfies the growling in your stomach. The second piece you eat may satisfy some hunger, but much of that was addressed by the first piece? What about by the time you eat the third piece? How useful is that fourth piece toward addressing hunger? Let's assume you bought one piece at a time. After you eat each piece, you go back to the counter and order another. Will that fourth piece be as valuable to you as the first? Probably not. If you could assign a value to each piece of pizza in satisfying your hunger, it might look like this:

Thus, we could say the marginal value of each piece of pizza declines as you consume each additional piece. The sum of value in an 8 slice piece of pizza, then, is $5.12 ($1.35 + $1.00 + $0.63 + $0.35 + $0.18 + $0.08 + $0.04). In other words, the satisfaction/value one gets out of one more - marginal - piece of a good or service is less than the use or value one could obtain by satisfying another unmet need. Perhaps a drink to wash down the pizza?

The goal of a person buying goods and services is to satisfy as many needs as possible using marginal utility to help him or her. Of course, value is difficult to measure. Can you measure how much you like ice cream? Probably not in a quantifiable way. One way to measure value is through prices in a free market. A seller of pizza could drop the price of the 9th piece of pizza to near zero and it is unlikely someone who just 8 pieces would buy it. Thus, one can imply that prices help buyers prioritize how they will satisfy their needs based on the current unmet needs.

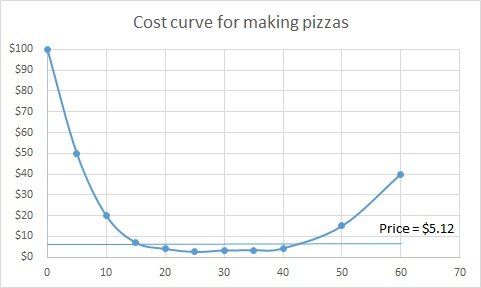

Marginal utility helps buyers decide how much and what to buy. What do sellers use to decide how much and what to sell? They use the same notion of margin to evaluate the costs of producing one more product or service. Economists refer to this as marginal cost. The pizza shop will benefit from selling many pizzas at $5.12. How many should it sell at this price?

Sellers produce goods and services to earn a profit. Profit is money earned above what it costs to make the good and service. Costs for pizza include the dough, cheese, sauce, a store, people to assemble the pizzas, an oven, heat, light, and so on. If the store only made one pizza, its cost would be so high it could not afford to sell the pizza at $5.12. This is because all the costs would be higher than the revenue from the pizza, so the store would lose money. Let's say the cost to make one pizza is about $100. Selling only one would mean $5.12 -100 = $94.88 loss. Who would want to pay that $94.88 to sell a pizza to help someone satisfy a hunger need? The pizza store owner has needs to satisfy, too. The more pizzas the store could make and sell, the more those costs could be divided by the number of pizzas. For example, at 30 pizzas, the total costs might be $120 (because more materials are needed to make more pizza). $120 / 30 = $4. At this quantity, the pizza store owner makes $5.12 - 4 = $1.12 profit per pizza sold. The pizza maker cannot make an unlimited supply of pizzas, though. At some point, the owner would have to hire more people to help make the pizzas, which raises costs. The pizza owner thinks about the cost of producing just one more pizza to see if it is worth it (valuable). This is marginal cost and it might look something like this:

Once the marginal cost of making one more pizza gets to the price at which the store sells the pizza, no more pizzas will be made, unless the store can raise the price. However, the pizza store down the street might keep its price at $5.12, so sales might be lost to that store. Thus, sellers also prioritize by price - and cost - to determine what to offer for sale as a means to maximize profits.

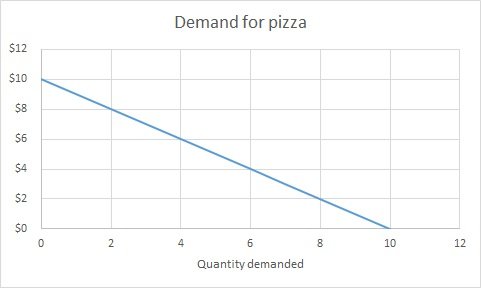

Each buyer's preferences for a good or service reflects his or marginal utility for that good or service. The demand for a good or service has an inverse relationship. That is, the lower the price, the more likely a person will buy the good or service. Economists refer to this as the law of demand. This is true to the extent the person's marginal utility is higher than the next unsatisfied need. This demand for a product or service also includes a time preference. The same good or service may be more or less valuable, depending on whether you can wait for it. If you want the item now, you may end up paying more for it because there is the value of the product or service itself and there is value in the timing of when you receive it.

A graph of this inverse relationship between price and quantity demanded of pizza might look like this:

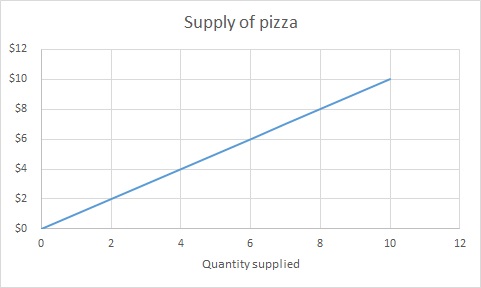

The seller's choices between how much of a good or service to supply and at what price is a direct relationship. That is, as the price a buyer is willing to pay goes up, the seller is willing to sell more of that good or service. Economists refer to this as the law of supply. A graph of this direct relationship between price and quantity supplied of pizza might look like this:

Back to the notion of the Invisible Hand. These supply and demand relationships reflect the value buyers and sellers see in a given product or service. One way economists measure value in the marketplace is the exchange price; that is, the agreed upon price that buyers and sellers are both willing to exchange currency for a product or service.

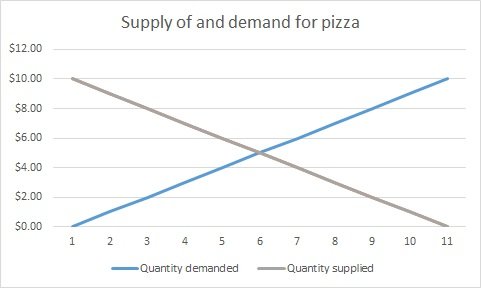

In a free market, no one sets the specific price; rather, it is the intersection of the buyer's mix of quantity demanded - based on marginal utility - and the seller's mix of quantity supplied - based on marginal cost. The exchange - or market-clearing price reflects the intersection of the demand curve - one will buy until price exceeds value - and the demand curve - one will sell until cost exceeds price, including profit. A graph of this intersection between quantity demanded and quantity supplied of pizza might look like this:

The market-clearing price at this intersection is one in which buyers and sellers are both content to exchange goods and services for money. A free marketplace is one that has minimal significant restrictions that limit voluntary decisions about what to buy and sell and at what price. This marketplace is also efficient because it represents buyer preferences, based on how well goods and services satisfy needs. It is also efficient because it represents the exact amount of goods and services supplied, based on the marginal cost of production.

So, while each individual or company makes decisions primarily with their "selfish" interests in mind, the total of these actions in the marketplace results in needs being met at an efficient price, and at a quantity that matches what sellers are willing to provide at a given efficient price. Each buyer and seller has a choice to offer or buy something or not. The decisions regarding the choice are made at the margin in the marketplace.

Watch in the video below how the store owner explains to Beth what she believes to be the sources of value in the handcrafted item. Beth counters with an alternative value for a set, one that includes a discount. They both agree, and both are satisfied with their voluntary exchange. Beth gets the cups, the shop owner gets the cash. This is also an example of offer and acceptance covered in the next chapter.

Discussion Questions:

Click to continue to the next chapter

Property Rights, the Rule of Law, and Contracts